Merkel Joins Sarkozy’s Call for Carbon ‘Border Tax Adjustment’ (Deutsche Welle)

Search Results for: border tax adjustment

Trade Expert Is Latest to Endorse Border Adjustments to Carbon Taxes

Border tax adjustments (“BTA’s”) — tariffs imposed on imported carbon-intensive goods with corresponding rebates of carbon taxes on domestically-produced goods destined for export — are one of the more technical issues in carbon tax policy. They’re also controversial; some analysts warn of trade wars or lengthy trade litigation in the World Trade Organization over a carbon-tax with BTA’s. But stay with us as we report on a new paper detailing two routes by which WTO rules would unequivocally support national carbon taxes with border tax adjustments and thus offer a route to a harmonized global carbon price.

Typhoon Haiyan Underscores the Urgency of Global Action to Curb Global Warming

The paper, published last July by the German Marshall fund of the United States, the American Action Forum and Climate Advisers, is hardly the first to reach such conclusions. In recent years, journal articles from leading academics including Joost Pauwelyn (Duke Univ. Law, 2007 & 2012), Gilbert Metcalf & David Weisbach (Harvard Envt’l Law, 2009), and Carolyn Fisher & Alan Fox (RFF, 2009) have pointed to the potential for BTA’s to create incentives for globally-harmonized carbon taxes. But the July paper, “Changing Climate for Carbon Taxes, Who’s Afraid of the WTO?,” comes from an even more prominent and unimpeachable source.

The author, Jennifer Hillman, a German Marshall Fund senior transatlantic fellow, is one of the world’s leading trade experts. Hillman served for four years as counsel to the WTO Appellate Body (the “Supreme Court” of trade law) and, prior to that, served an eight-year term as a U.S. International Trade Commissioner. From 1995-1997, as General Counsel to the Office of United States Trade Representative, she oversaw U.S. government submissions in dispute settlement cases before both WTO and NAFTA.

So Hillman is an impressive messenger. Here’s why her conclusions are important, and why BTA’s are a crucial element of an effective U.S. carbon tax.

For carbon taxes to form the cornerstone of policies to de-carbonize the world economy, carbon pricing will need to “go global.” But without border tax adjustments, unilateral U.S. climate policy won’t necessarily lead to global emissions reductions (due to “off-shoring” of factories) and could disadvantage domestic energy-intensive business.

BTA’s offer a way to not only protect domestic energy-intensive industry but also provide carrots and sticks to induce our trading partners to enact their own carbon taxes and to prevent “carbon leakage” from relocation of energy-intensive industries. Moreover, a WTO-based process could obviate the U.N. Kyoto Protocol (“COP”) meetings where nations have wrangled for almost two decades to allocate the Earth’s dwindling carbon “budget.” Instead, the U.S. (or any large trading bloc) could simply enact a carbon tax and use WTO-sanctioned border tax adjustments to induce other nations to follow.

The General Agreement on Tariffs and Trade (GATT) functions as the “constitution” of the World Trade Organization in its mission to foster global trade. Hillman shows that GATT Articles II.2 and III.3 empower countries to impose taxes on imports provided they do not exceed the taxes imposed on “like” domestically-produced goods. (Historically, tax systems that have run afoul of Article II and III have been discriminatory attempts to favor domestically-produced goods by imposing higher tariffs on foreign-produced goods.) GATT allows taxes based on the production process — in the case of a carbon tax the “carbon intensity” of the production process. This would require data on production processes abroad, which may be difficult to obtain. Hillman suggests that, absent such data, WTO would accept an assumption that an imported product’s carbon intensity is similar to that of a like domestically-produced product. (Companies producing goods less carbon intensively than U.S.-produced equivalents could petition for reductions in their border tax adjustment.)

Hillman offers a second avenue for BTA’s via GATT Article XX, which authorizes WTO members to adopt policies to protect human, animal or plant health or to conserve exhaustible natural resources. The general WTO policy of non-discrimination and non-interference with international trade would also apply to tariffs adopted pursuant to Article XX.

Hillman also recommends a rebate of carbon taxes paid on exported goods to ensure that domestic producers selling goods into non-carbon-taxing countries aren’t disadvantaged. She concludes that WTO should permit such rebates so long as they don’t exceed the carbon tax actually paid.

Hillman concludes:

Policymakers have sufficient latitude with this [WTO] framework to design and implement a carbon tax system that represents a good faith effort to reduce carbon emissions while encouraging all other countries to cut their emissions too, all while preserving the competitive position of U.S. companies. Policy makers can be bold; the WTO will recognize genuine climate change measures for what they are and is unlikely to find fault with such measures, provided they do not unfairly discriminate in favor of U.S. companies.

Photo: Jun Tokumori (Flickr)

New Senate bill would price CO2 at $54/metric ton and tax some particulates, SO2, NOx

This post was updated, and its headline slightly altered, on July 13, 2021.

A bill introduced in June by Senators Sheldon Whitehouse (D-RI) and Brian Schatz (D-HI) envisions a hefty price on U.S. carbon dioxide emissions from all sources along with pollution charges on the three primary “criteria” air pollutants — particulates, sulfur dioxide and nitrogen oxides — from large stationary sources near environmental justice communities.

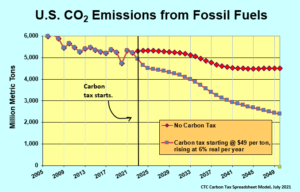

The Save Our Future Act (101-page downloadable pdf) prices CO2 emissions at $54 per metric ton, equivalent to $49 per U.S. (short) ton, starting in 2023, with the price rising each year by a percent equal to 6 percentage points on top of the rate of general inflation.

The bill also proposes to charge emissions of fine particulates, nitrogen oxides and sulfur dioxide from qualified “major sources” (a legal term defined at 42 U.S.C. 7661) located within a mile of any environmental justice community (see definition and discussion further below). In addition, a border adjustment mechanism would prevent carbon leakage and ensure fairness for U.S. manufacturers, according to a press release from Sen. Whitehouse’s office, while an “environmental integrity mechanism” would raise the charges on CO2 and other greenhouse gases if needed to keep shrinking emissions fast enough to meet a 2050 net zero target.

Pushing the Envelope

The Whitehouse-Schatz bill pushes the envelope of carbon tax legislation. The starting price of $49/ton — pegged to OMB’s conservative estimate of the social cost of carbon — represents a new high. So does the annual increase rate of general inflation plus 6%. Both figures surpass the Climate Leadership Council’s long-standing proposal to start pricing CO2 at $40/ton and raise that price 5% faster than annual inflation (to be fair, the council’s 2017 price base translates to $45/ton or more in 2023, the Whitehouse-Schatz bill’s start year).

Modeling by CTC suggests the Save Our Future Act will cut CO2 34% below 2005 levels in 10 years (without counting ancillary charges on PM-2.5, SO2 and NOx).

The Save Our Future Act is co-sponsored by Senators Martin Heinrich (D-NM), Kirsten Gillibrand (D-NY), Jack Reed (D-RI), Chris Murphy (D-CT), and Dianne Feinstein (D-CA). The Whitehouse press release says the bill is supported by the Utility Workers Union of America, the New York City Environmental Justice Alliance, New York Lawyers for the Public Interest, The Nature Conservancy, Environmental Defense Fund, National Wildlife Federation, American Sustainable Business Council, Citizens Climate Lobby, Clean Air Task Force, and the World Resources Institute, although sources have reported that neither of the New York groups have formally endorsed it.

We ran the CO2 price in the Save Our Future Act through CTC’s carbon tax model (which you may download via this link). The results, shown above, indicate that the bill won’t fulfill its stated objective to cut carbon emissions in half within a decade, though, to be fair, our modeling doesn’t reflect additional impacts from the prices on the three localized pollutants. Nor does our model capture the likely low-hanging fruit of curbing emissions of methane and other greenhouse gases.

Still, the price-compounding built into the bill limits its efficacy somewhat; even the unprecedented proposal to raise the rate 6% faster than inflation doesn’t boost the price nearly as fast as a straight-up $10/ton annual increment. (Simple math suggests that, with 2% annual inflation, the price won’t spin off annual increments of $10/ton or more until it has reached $125/ton.)

Revenue Treatment

How carbon revenues are used has become central to carbon taxing’s equity and politics. The following four bullet points, taken from the Whitehouse press release, summarize the Save Our Future Act’s proposed treatment:

- Environmental justice communities: The bill would invest roughly $255 billion over 10 years in existing energy affordability, pollution reduction, business development, career training, and tribal assistance programs.

- Fossil fuel workers and communities: The bill would invest roughly $120 billion over 10 years in economic development, infrastructure, environmental remediation, assistance to local and tribal governments, and wage replacement, health, retirement, and educational benefits for coal industry workers who lose their jobs.

- Assistance to states: The bill would fund $10 billion in annual block grants to states and tribes to defray expenses associated with climate change.

- Checks to low- and middle-income families: Consistent with the means testing thresholds established for pandemic relief checks in the American Rescue Plan, every eligible adult would receive $800/year and every eligible dependent $300/year, distributed in biennial installments.

Provisions #1 through #3 together would absorb around $500 billion over the law’s first decade, out of the total $4 trillion in revenue that CTC’s model indicates the Save Our Future Act will generate during that time. The difference between those figures — some $3.5 trillion total — pays for the dividend checks noted in provision #4.

The proposed allocation of the vast majority of revenues to the dividends presumably is what delivered support from Citizens Climate Lobby, the national grassroots organization that for the past decade has relentlessly pursued the idea of returning carbon-tax revenues as dividends to U.S. households. Provisions 1 through 3 clearly are designed to win backing for the bill from justice-oriented climate advocates.

Local Air Pollutants

Environmental justice is also evident in the bill’s novel proposal to charge for emissions of fine particulates ($38.90/lb), NOx ($6.30/lb) and SO2 ($18/lb), with those prices rising at the rate of inflation, from qualified “major sources” (a legal term defined at 42 U.S.C. 7661) located in or no more than a mile from an environmental justice community. Our preliminary calculations suggest that all fossil-fuel power stations 25 megawatts or larger, even those with modern combined-cycle technology burning methane gas, would meet the statutory criteria, provided they are sited directly proximate to a community of color.

Other large stationary polluters such as oil refineries, chemical plants and perhaps oil and gas extraction and processing facilities might also qualify. (We are awaiting details from Sen. Whitehouse’s office.) We estimate that coal-fired power plants would be charged for their “local” pollutants at a rate averaging around 5 cents per kWh generated, a fee that would effectively duplicate (i.e., double) the direct impact of the initial $49/ton carbon tax. Gas-fired power generators, in contrast, would pay only around 2/10 of a cent per kWh, on account of their sharply lower emission rates for conventional pollutants, relative to coal. (You can see our assumptions and calculations in the Local Pollutants tab of our carbon-tax model.)

Prospects

Prospects aren’t bright for the Save Our Future Act in the current Congress. The persistence of the Senate filibuster means that 60 out of 100 senators must approve the bill; yet opposition is virtually guaranteed from almost all 50 Republican senators along with Sen. Joe Manchin (D-WV) and perhaps a few other Democratic senators. Not only that, the Biden White House is unlikely to put its muscle behind the bill, for reasons we laid out earlier this year in our post, Playing the Long Game for Carbon Fee-and-Dividend:

Razor-thin House and Senate margins simply don’t allow for hot-button measures like carbon pricing that might jeopardize other elements of the package in addition to failing on their own. Biden’s task, as he knows full well, is to pass bold, progressive, popular legislation to help Democrats expand their Congressional majorities in 2022 and 2024 and give him a thumping second-term mandate to boot. Then, and only then, can he risk a carbon tax.

Still, let’s credit the Save Our Future Act for pushing the envelope on carbon taxing on the twin key fronts of tax design and revenue treatment. Kudos to Senators Whitehouse and Schatz for seeking support from a diverse set of environmental and justice campaigners. The bill underscores the importance of solidifying a pro-climate Congress to enable such forward-thinking bills to be seriously considered during the second half of the Biden term.

Where Carbon Is Taxed (Some Individual Countries)

This page reports on carbon taxes that have been enacted (and in one case, enacted and withdrawn) in:

Canada has its own page, where we summarize its nationwide carbon price and also report in detail on British Columbia’s carbon tax, the Western Hemisphere’s (if not the world’s) most comprehensive and transparent carbon tax.

European Union: Emissions Trading System

The European Union (EU) implemented a carbon cap-and-trade system in 2005. The EU Emissions Trading System (ETS) is the world’s first international emissions trading system, operating in all EU member countries plus Iceland, Norway, and Liechtenstein.

The EU ETS covers over 10,000 stationary emitters — mostly power stations and industrial plants. It also covers domestic and intra-EU air travel. In toto, the ETS covers around 40 percent of the EU’s greenhouse gas (GHG) emissions, making it the largest carbon cap-and-trade program in the world, covering approximately 1.5 billion metric tons of CO2 per year.

For much of its existence, the ETS was largely ineffectual because its emissions caps were too high and granted large numbers of free allowances to big polluters. Concern about carbon leakage — polluters from the EU potentially going elsewhere to do their polluting, hence, “leaking” carbon from the EU — drove the EU to implement free allowances as its primary method of allocation back in 2005. As a result, polluters obtained large numbers of allowances — in 2013, manufacturers received 80% of their allowances for free — and many were able to maintain a surplus.

Compounding the problem of giveaways, the EU grossly overestimated future CO2 emissions in setting the cap amounts, resulting in a too-high number of allowances. In the first phase of the EU ETS, from 2005-2007, only three member states had caps lower than baseline 2005 emissions levels. And with the 2008 financial crisis driving emissions down, the caps were rendered even more useless.

Background

In December 2019, the European Commission — the executive branch of the EU — introduced the European Green Deal, an ambitious climate policy package with the general goal of at least 50% GHG emissions reductions by 2030 and carbon neutrality by 2050. The European Green Deal represents the EU’s main legislative effort to meet its commitments under the Paris Climate Agreement. The Green Deal included the ETS as an integral part of its action plan.

In 2020, the EU expanded to a 55% reduction its commitment to reduce emissions 40% from 1990 levels by 2030 and. The ramp-up came in December 2020, following all-night negotations in which the EU committed to helping coal-heavy countries like Poland meet individual-country commitments.

The U.K.’s concurrent exit from the EU and ETS caused a substantial exit of low-carbon power producers, resulting in an increase in average carbon contents for the remaining EU power producers. It’s not yet clear how these changes will play out, as the U.K. has not announced plans to link with any other carbon trading systems.

How the ETS Works

The European Trading System implements an emissions cap for the overall volume of GHG that may be emitted by covered airlines, power plants and factories. Emitting companies purchase at auction — or receive — tradable allowances, the total number of which is capped at a level that steadily decreases each year. Since 2013, the emissions cap has applied to the EU as a whole, not individual countries. The current cap for 2021 on GHG emissions from these stationary installations is 1.57 billion tonnes per year, or roughly half of 2019 CO2 emissions for the entire European Union, including the U.K.

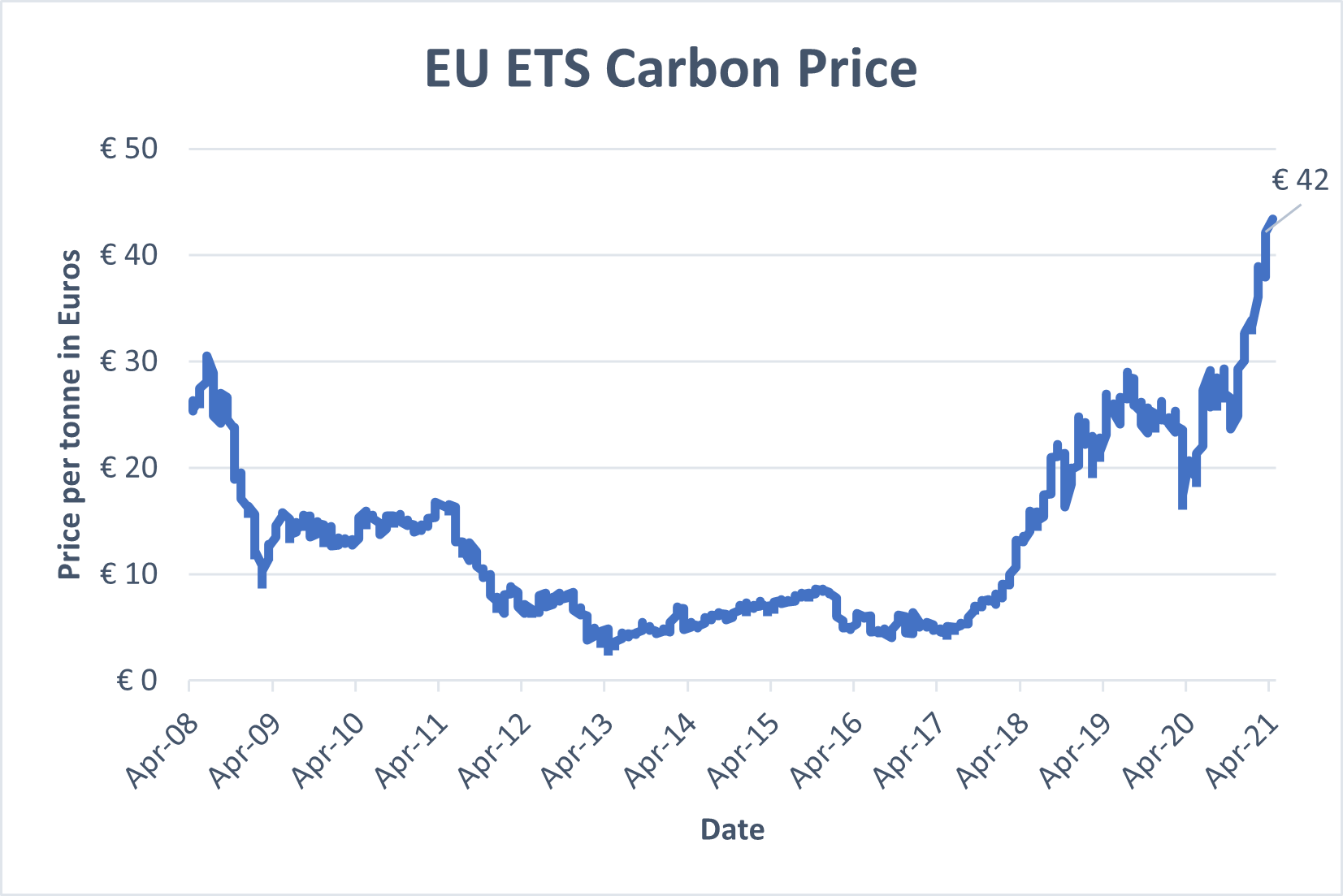

Data from https://ember-climate.org/data/carbon-price-viewer/

The price of a carbon allowance has roughly doubled in the past several years, reaching a high of nearly €43 in March 2021. BloombergNEF (New Energy Finance) projects that prices will hit €100 by 2030. The higher price levels enable the ETA to “arguably serve its purpose by making it too expensive for emitters of fossil fuels to continue business as usual,” as reported in early 2021 by Alessandro Vitelli of Montel News.

Since January 2019, the EU ETS has included a market stability reserve (MSR), which maintains any surplus of allowances, allowing for adjustments to the supply of allowances up for auction, if needed. Unallocated allowances are transferred to the reserve, which is operated under strict rules that bar meddling by the Commission or Member States.

Phases

The ETS’s 15-year tenure to 2020 may be divided into three phases.

- Phase 1, from 2005-2007, served as a pilot of “learning by doing.” During that phase, about 12,000 installations received permits to emit about 2.2 billion tons of CO2, nearly half of EU CO2 emissions at that time. Most allowances were given for free.

- In Phase 2, 2008-2012, the cap on allowances was reduced by 6.5% compared to 2005. Phase 2 aligned with the first commitment period of the Kyoto Protocol, when countries in the EU ETS had to fulfill commitments to reduce emissions by an average of 5% below 1990 levels. (The EU and its member countries ended up cutting emissions by 8% below 1990 levels.) Several countries held auctions.

- Phase 3, 2013-present, saw the application of a single, EU-wide cap on emissions instead of the previous system of national caps. Auctioning replaced free allocation as the default method of allowance allocation. Phase 3 also brought more sectors and gases under the EU ETS umbrella. During this phase, the EU-wide cap on stationary installations decreased by 1.74% each year.

For Phase 4, from 2021-2030, the Commission revised and strengthened the EU ETS in 2018. The overall number of emission allowances will now decrease at an annual rate of 2.2%, instead of 1.74%. However, significant amounts of free allowances remain, ostensibly to combat carbon leakage. The EU will still give 100% free allocation to sectors at the highest risk of relocating production outside the EU. For industries less likely to flee, free allocation will be phased out, from a maximum of 30% in 2026 to zero by 2030. Overall, the EU predicts 6 billion free allowances will be granted from 2021-2030.

Impact

The EU ETS’s specific targets are to reduce GHG emissions by 21% between 2005 and 2020, and by 43% by 2030.

Total EU emissions of greenhouse gases fell by 23 percent from 1990 to 2018, according to the European Commission. Emissions from ETS sectors alone fell 33% from 2005-2019.

Carbon leakage

In its Green Deal statement, the European Commission addressed the concern that countries across the world will continue to have “differences in levels of ambition,” by pledging to propose a carbon border adjustment mechanism as an alternative to the ETS’s carbon-leakage measures. As Inside Climate News explains carbon border adjustments:

Economists have long suggested that there’s a way to break that global impasse [on climate action] — and that’s to treat carbon like any other international trade dispute. Impose tariffs or quotas on imports from countries that have given their manufacturers an unfair advantage of uncontrolled carbon emissions.

In March 2021, the European Parliament adopted a resolution favoring a carbon border adjustment mechanism. The European Commission will propose legislation in June 2021.

United Kingdom

The United Kingdom — England, Scotland, Wales and Northern Ireland — has maintained a carbon tax since 2013. Technically, the tax is a “carbon price floor” (CPF) that functions as the minimum price that fossil fuel producers pay for emitting CO2. The CPF applies to energy-intensive industries only and is not economy-wide.

There have been several calls lately to tax carbon emissions in the U.K. at a higher rate and on a broader scale. Grantham Institute researchers Josh Burke and Esin Serin argued in a fascinating Feb. 2021 opinion piece that carbon pricing should be enacted not as a stand-alone but “as part of a significant and broad package of post-COVID fiscal reforms.”

History

As a result of the 2008 Climate Change Act — passed with overwhelming support across parties — the U.K. was required to drastically reduce its carbon output according to five-year carbon budgets. Unsurprisingly, the U.K. — birthplace of classical economics and home base of Sir Nicholas Stern, the renowned economist who in 2007 famously called climate change “the result of the greatest market failure the world has seen” — turned to carbon pricing to carry part of the load.

In 2009, the Department of Energy and Climate Change released a report, “Carbon Valuation in UK Policy Appraisal: A Revised Approach,” detailing reasons to adopt a carbon price. Witnesses at the 2009-2010 Environmental Audit Committee’s report on Carbon Budgets called for a carbon price floor, but the Labour government opposed the idea. Then in 2010, the Coalition government consulted on proposals for a CPF, and the measure was introduced in the 2011 Budget for implementation in 2013. The 2011 Budget framed the CPF as a way to “drive investment in the low-carbon power sector” and “support the long-term stability of the public finances.” The government also said the CPF “achieves the right balance between encouraging investment without undermining the competitiveness of UK industry.”

When the carbon floor was introduced, the Confederation of British Industry and Renewables Energy Association were supportive, but the measure also found criticism from several sides that argued it was, by turns, ineffective, expensive, and uncertain for investors. But the government framed the tax as the best move for consumers, stating that the “market-based approach to pricing carbon provides the most efficient and cost-effective policy framework to meet our environmental goals.”

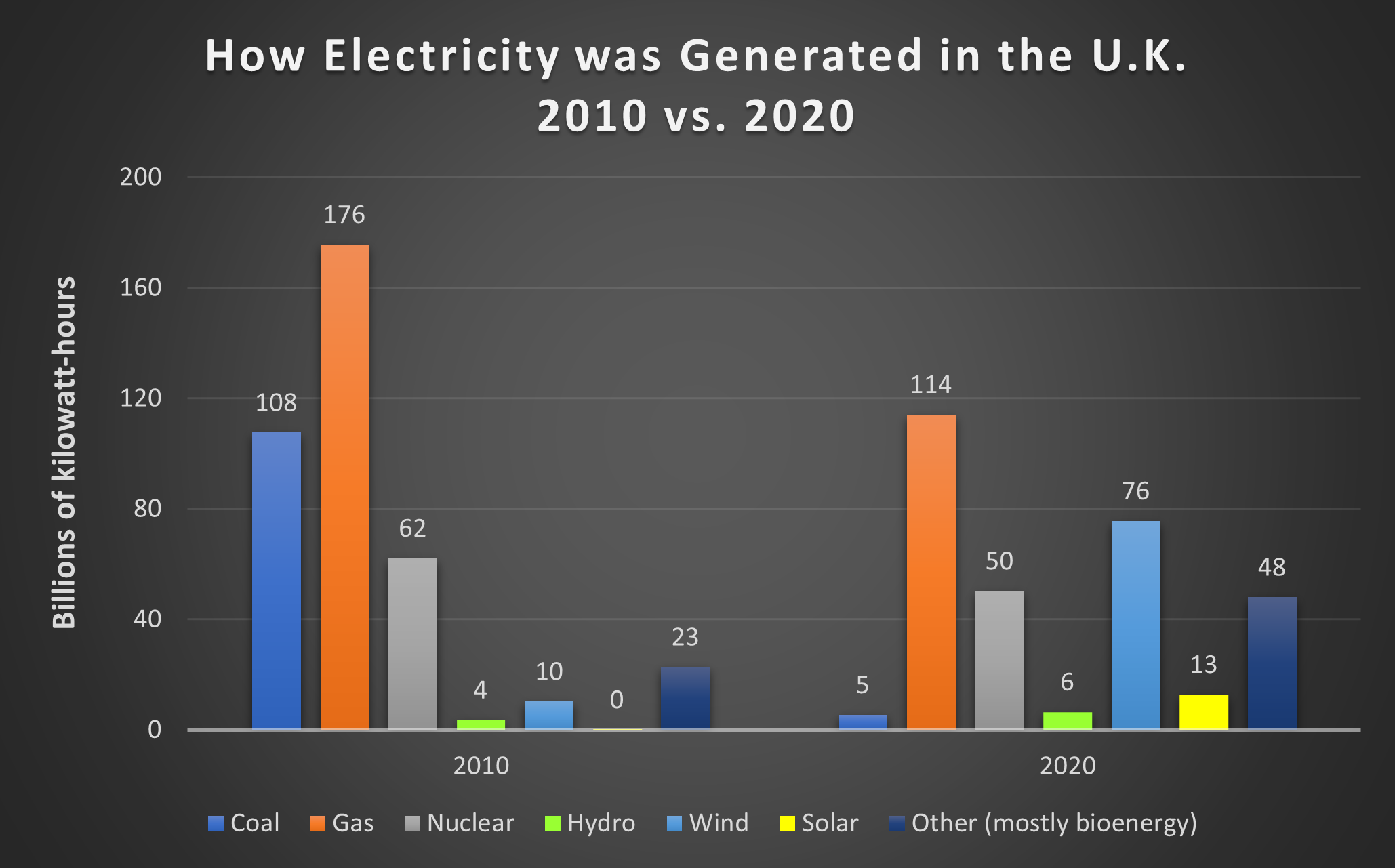

Data from U.K. Gov’t Energy Trends. Data exclude international aviation, shipping and emissions in producing imported goods.

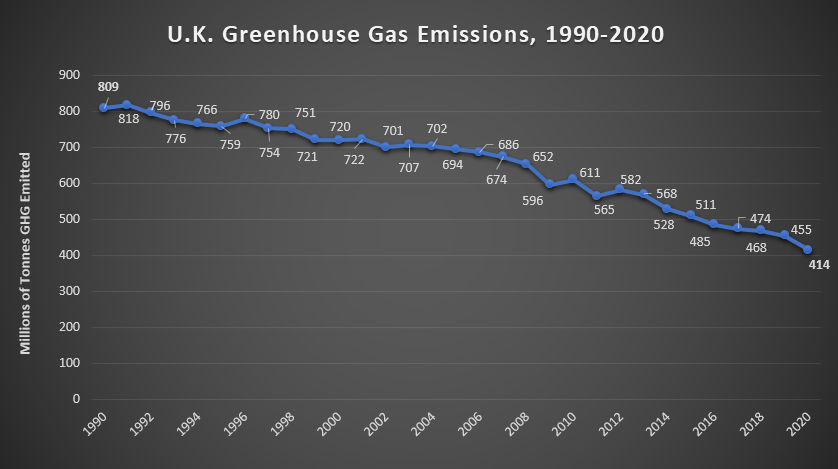

Less than 10 years after implementing the CPF, the U.K. is halfway to meeting its goal of net zero greenhouse gas emissions by 2050. U.K. GHG emissions in 2020 were 51% below 1990 levels, putting the country mathematically on track to reach net zero by 2050.

30 Years of Falling Emissions

The first graph makes clear that this 2020 milestone is only slightly due to the COVID-19 pandemic. The 2020 decline in emissions, though severe, roughly 40 million tonnes, was no greater than that in 2014 (also 40 million tonnes) and was less than the 56 million tonne drop in 2009, during the severe recession. Emissions fell in almost every year from 1990.

Data from Department for Business, Energy & Industrial Strategy: Dataset for quarterly and monthly supply and consumption of electricity, Table 5.1.

The anticipated recovery from COVID-19 will, of course, provoke a partial rebound in emissions. The national government’s March 2021 Industrial Decarbonisation Strategy specifies that industrial emissions must fall by two-thirds before 2035 to enable the U.K. to meet its Dec. 2019 pledge — the first by a major economy in the world — to reach net-zero GHG emissions by 2050.

What accounts for the huge drop in U.K. greenhouse gas emissions from 1990 to 2019? Carbon Brief credits three changes for around 90% of the decline:

- Electricity that doesn’t rely on coal – 43% of electricity was generated by renewables in 2020 (“renewables” does not include nuclear power, but it does include wind, hydro, solar, and bioenergy).

- Cleaner industry and a shift away from carbon-intensive manufacturing.

- A pared-down, cleaner fossil fuel supply industry.

It’s important to note, however, that a considerable amount of U.K. “renewable” electricity is generated by burning biomass, i.e. wood pellets. Inclusion of bioenergy as a renewable source of energy is at best contentious and more likely a scam, as journalist Michael Grunwald pointed out in his March, 2019 expose in Politico.

U.K. Carbon Pricing: Details

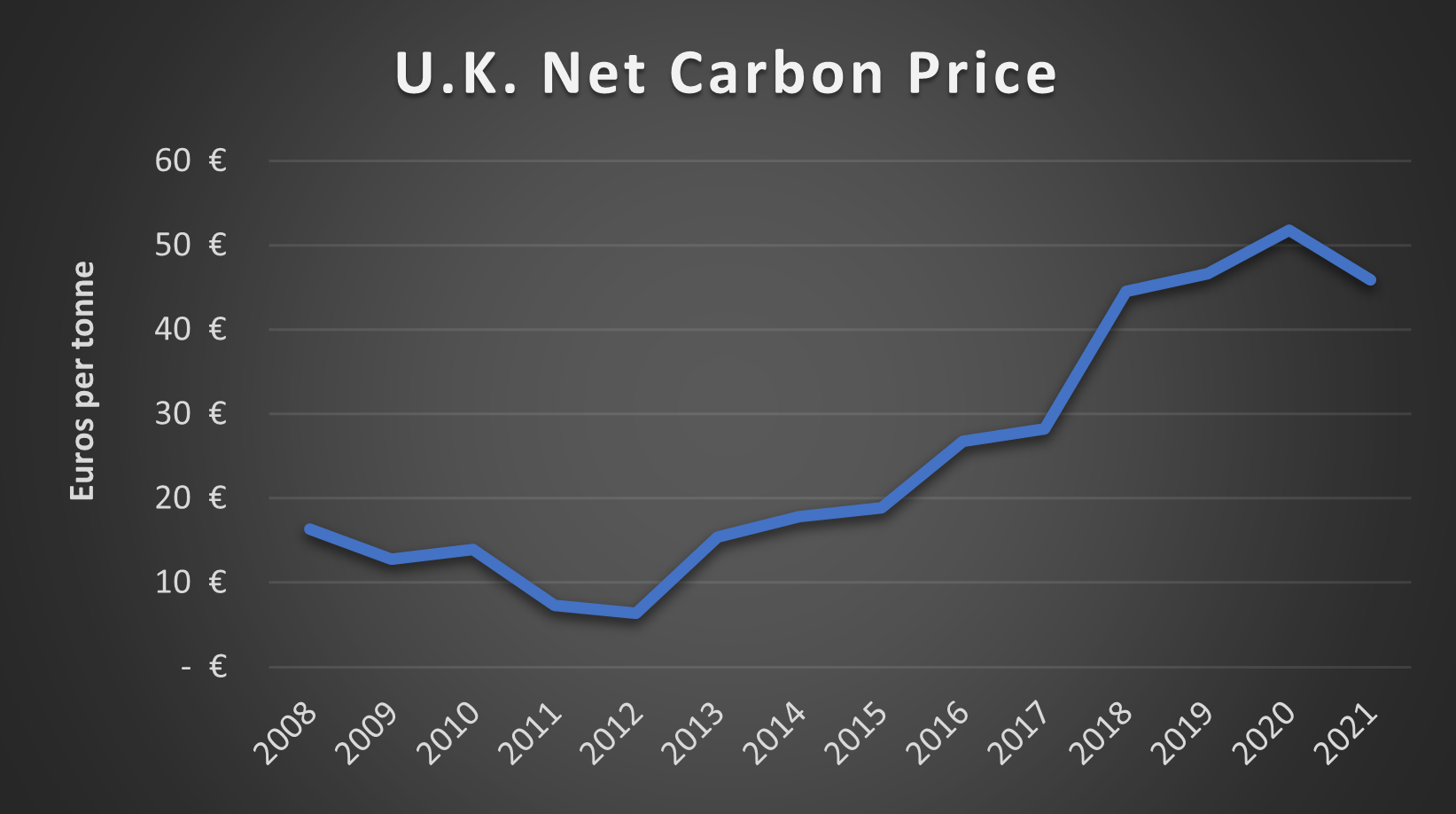

Data from https://ember-climate.org/data/carbon-price-viewer/ and https://commonslibrary.parliament.uk/research-briefings/sn05927/

Initially priced at £16/tonne in 2013, the U.K.’s carbon price floor (CPF) was set to increase to every year, hitting £30/tonne by 2020 and £70/tonne in 2030, but was capped in 2015 at £18.08/tonne until 2021 (20.40 euros at the 2015 exchange rate). The CPF has impacted the generation fuel mix significantly; coals share fell from 41% in 2013 to less than 8% in 2017.

Brits sometimes call their CPF a “top up” tax since it was intended to top up European carbon pricing in the form of the EU emissions trading scheme (ETS). The U.K. finished its Brexit transition from the EU at the end of 2020, creating the need for a new, non-EU emissions trading scheme (ETS).

The U.K. announced in February 2021 that it would launch its own carbon trading scheme in May 2021. The U.K. government says their ETS replaced the UK’s participation in the EU ETS as of January 1, 2021, but the first U.K. ETS emissions auctions will not begin until May 19, 2021.

According to Auctioning Regulations released in February, bids will follow a minimum Auction Reserve Price (ARP) of £22/tonne when they begin in May, but the price will increase: “The government will consult on its intent to withdraw the ARP as part of the planned consultation to appropriately align the U.K. ETS cap with a net zero trajectory which will be launched later this year.”

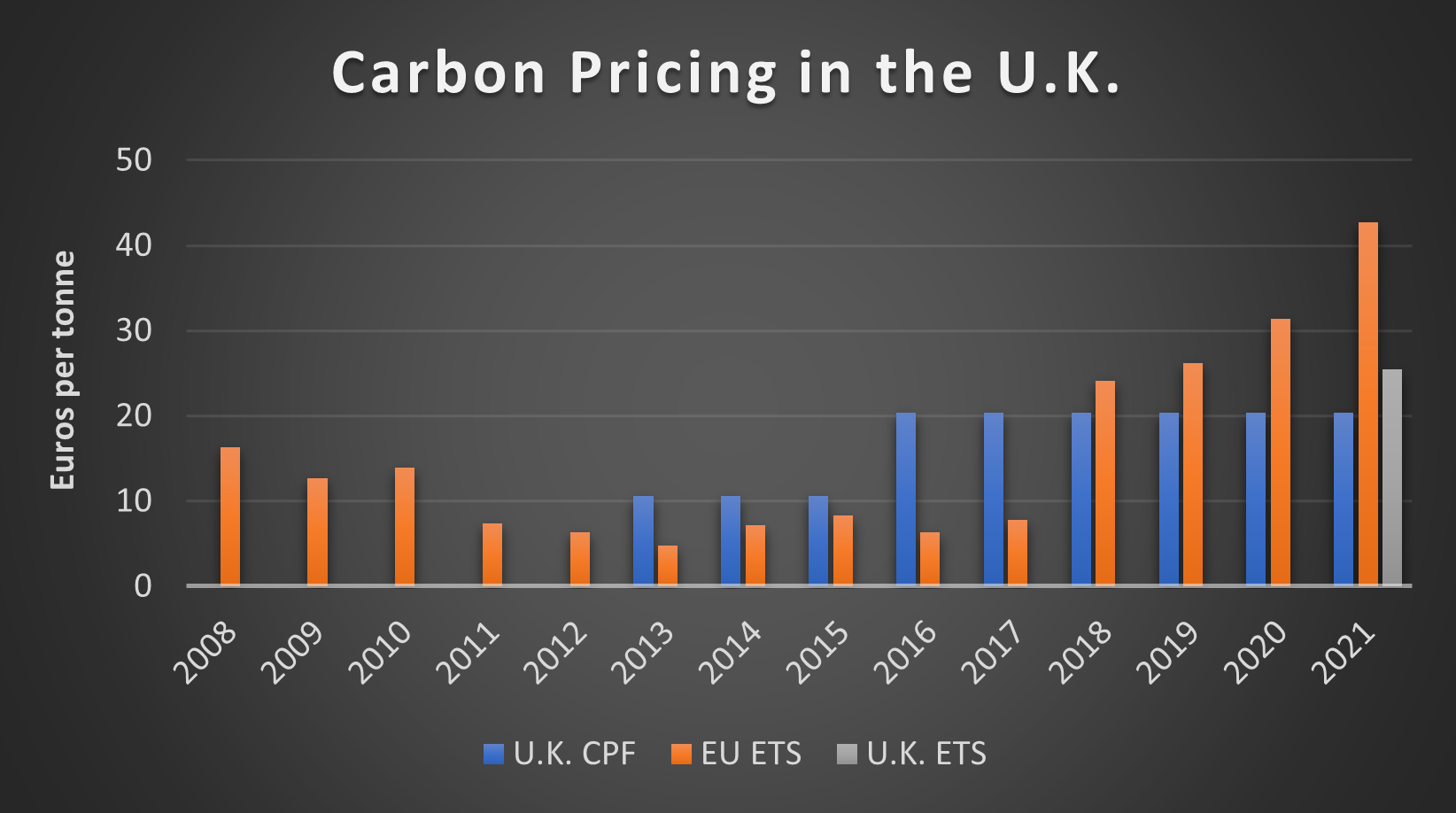

Data from https://ember-climate.org/data/carbon-price-viewer/ and https://commonslibrary.parliament.uk/research-briefings/sn05927/

The floor for the U.K. ETS was initially set to 15 pounds but raised to 22 pounds per tonne, perhaps following some form of the logic suggested by climate advocacy group Ember: “The EU ETS has averaged a price of around £22/t (€25/t) over the last two years, so it would make sense to set the U.K. carbon price floor to at least that level, especially with further reform to strengthen the EU ETS price due in the coming year.”

The U.K. government stated in the Autumn Budget 2017 that they were “confident that the Total Carbon Price, currently created by the combination of the EU Emissions Trading System [of 7.78] and the Carbon Price Support [of 20.40], is set at the right level, and will continue to target a similar total carbon price until unabated coal is no longer used.”

Ireland

(Thanks to Wesleyan University environmental studies major Nicholas J. Murphy for expanding this section in July 2015.)

Ireland enacted a carbon tax in 2010 under a coalition government of its Green Party, Fianna Fáil (one of Ireland’s two mainstay center-right parties) and the Progressive Democrats. Originally designed to provide a double dividend by offsetting income taxes, the revenue was re-allocated to satisfy the diktats of the Troika — the triumvirate of the European Commission (EC), International Monetary Fund (IMF) and European Central Bank (ECB) that administered the austerity policies on EU member nations bailed out during the 2008 debt crisis. (See OECD working paper on Ireland’s Carbon Tax and the Fiscal Crisis.)

The effect is arguably similar, since income taxes would have had to rise, absent the carbon tax revenues. Frank Convery, an economist at University College Dublin considered the foremost expert on Ireland’s carbon tax, writes enthusiastically:

Ireland is a pioneer in the implementation of a carbon tax. This has allowed us to avoid (more) increases in income tax which would have further reduced disposable income, increased labour costs and destroyed jobs. It is also facilitating us in meeting our very demanding legally binding obligations to reduce greenhouse gas emissions, and provides support for the creation of new jobs in improving energy efficiency and growing the low carbon economy.

Ireland’s carbon tax covers nearly all of the fossil fuels used by homes, offices, vehicles and farms, based on each fuel’s CO2 emissions. It began in 2010 at €15/ton and rose to €20/ton in 2012, where it remains today. Solid fuels (coal and peat) were added in 2013 at €10/ton after concerns from agricultural interests were resolved, and that price has since risen to match the €20 price on other fuels. The tax generates roughly €100 million in revenue per €5 of tax, meaning it currently draws about €400 million annually.

The carbon tax has been complemented by other environmental taxes based on vehicle fuel efficiency and domestic landfill waste, as New York Times environmental correspondent Elisabeth Rosenthal reported in Dec. 2012, in Carbon Taxes Make Ireland Even Greener:

Over the last three years, with its economy in tatters, Ireland embraced a novel strategy to help reduce its staggering deficit: charging households and businesses for the environmental damage they cause. The government imposed taxes on most of the fossil fuels used by homes, offices, vehicles and farms, based on each fuel’s carbon dioxide emissions, a move that immediately drove up prices for oil, natural gas and kerosene.

Household trash is weighed at the curb, and residents are billed for anything that is not being recycled. The Irish now pay purchase taxes on new cars and yearly registration fees that rise steeply in proportion to the vehicle’s emissions.

Environmentally and economically, the new taxes have delivered results. Long one of Europe’s highest per-capita producers of greenhouse gases, with levels nearing those of the United States, Ireland has seen its emissions drop more than 15 percent since 2008. Although much of that decline can be attributed to a recession, changes in behavior also played a major role, experts say, noting that the country’s emissions dropped 6.7 percent in 2011 even as the economy grew slightly.

Notably, the Irish carbon tax was designed to fill gaps left by the European Union Emissions Trading Scheme (EU ETS), which addresses only large polluting firms and accounts for only roughly 40% of emissions sources while being hampered by volatility. The case of Ireland demonstrates the potential for EU-wide cooperation in setting an effective harmonized price on carbon in preference to a piecemeal and volatile ETS.

The elements of Ireland’s carbon tax introduced in 2010 are specified in the Finance Act of 2010. (See Part 3 (Customs and Excise), Chapters 1 (Oil), 2 (Natural Gas), and 3 (Solid Fuels) for tax rates and other provisions.)

Ireland’s Vehicle Registration Tax is also partly emissions-based. A VRT Calculator on the Irish Tax & Customs website provides a means to estimate the amount of tax on a vehicle based on Make/Model/CO2 Emissions. Interestingly, the CO2-sensitive VRT has touched off a pronounced shift to diesel vehicles, which emit less CO2 but more of other pollutants with localized health impacts. Changes to the tax rate in Budget 2013 are detailed here.

Finally, the law firm Arthur Cox offers these useful guides ([1] & [2]) to Ireland’s carbon tax.

Australia

The widespread wildfires devastating much of Australia in the Southern Hemisphere’s 2019-2020 summer have drawn worldwide news coverage and cast that country’s retrograde official climate stance in appropriately harsh light. CTC’s blog post, Australia’s Brief, Shining Carbon Tax distilled and updated the information below and also revealed the stunning detail that the two years in which Australia had a national carbon tax, 2012-2014, saw dramatic drops in CO2 emissions, both absolute and relative to GDP (see graphic directly below, at left). As of this mid-January writing, however, no other media had picked up this finding.

The Liberal Party government of PM Scott Morrison has come under withering attack for hewing to the climate-denying line of the Murdoch-dominated press that alternately blames the fires on arsonists and wildland “mismanagement” while hand-wringing that unilateral action to curb Australia’s emissions would have little or no discernible impact because the country accounts for only 1 percent of global CO2. The Daily Beast has reported that James Murdoch, the media baron’s younger son, was sharply critical of Fox News and News Corp’s “climate-change denial,” while Australian union organizer James Raynes posted the ironic tweet shown at right.

Here’s how an Australia labor organizer lampooned his government’s “why bother” climate stance.

Our earlier coverage of Australia carbon taxing, though somewhat dated, is below. Be sure to read our Jan. 7 (2020) post.

Australia instituted a carbon tax on July 1, 2012 and repealed it two years later, on July 17, 2014. Both events were milestones. Though some countries, notably Sweden, have had longer-standing and stronger national carbon levies, Australia’s was the first explicit national tax on carbon emissions. The repeal was also precedent-setting, and predictably it has garnered far more global attention (and hand-wringing) than did the tax itself.

The tax level, $23 per tonne (metric ton), equated to $19.60 per U.S. ton of CO2, at the U.S.-Australian dollar exchange rate (1.00/0.94) in July 2014.

As recounted by Australian journalist Julia Baird in a 2014 NY Times op-ed, A Carbon Tax’s Ignoble End: Why Tony Abbott Axed Australia’s Carbon Tax, published a week after Australia’s Senate voted for repeal, the tax was a political stepchild, opposed by the country’s two major political parties, left-leaning Labor and center-right Liberal, and brokered by the Greens during a period of governmental stalemate in 2011-2012:

In 2010, the Labor prime minister, Julia Gillard, said she would look at carbon-pricing proposals, but also promised, “There will be no carbon tax under the government I lead.” Then, under pressure to form a minority government, she made a deal with the Greens and agreed to legislate a carbon price: a tax by any other name.

The heat, anger and vitriol directed at her as a leader — and as Australia’s first woman to be prime minister — coalesced around the promise and the tax. It grew strangely nasty: She was branded by a right-wing shockjock as “Ju-Liar,” a moniker she struggled to shake. The political cynicism surrounding the carbon tax certainly reduced Ms. Gillard’s political capital, but it was a perceived lack of conviction in the policy itself that damaged the pricing scheme’s credibility.

See also Australian ABC News’ superb Timeline of the tax’s torturous political path, posted in July 2014.

Predictably, the Times’ news dispatch, Environmentalists Decry Repeal of Australia’s Carbon Tax, cast the repeal as greens vs. economy, ignoring the reductions in carbon intensity in the power sector (which helped blunt the tax’s cost) as well as provisions that directed revenues to households to mitigate consumer impacts (see below).

Australia’s carbon tax also imposed climate-equivalent fees on methane, nitrous oxide and perfluorocarbons from aluminium smelting, and was collected from roughly 500 of the nation’s biggest emitters, according to the Big Pond Money blog. These included electricity generation, stationary energy producers, mining, business transport, waste and industrial processes; some (non-electric) industries were eligible to receive trade-exposure based assistance, according to the same source. Most if not all road transport fuel (i.e., petrol) was exempt. The tax level was indexed to inflation and rose from the initial $23.00 (Australian) per tonne to $24.15 per tonne in 2013 and $25.40 in 2014. Beginning July 1, 2015 the price was to be set by a cap-and-trade system linked to the EU ETS (whose price has fallen below $10/T CO2). PolitiFact Australia compared the size and breadth of its carbon tax with others around the world, neatly refuting the Liberal Party’s pejorative characterization of the tax as “the world’s largest.”

In May 2013, one of Australia’s major papers, the Age, reported that national electricity generation with highly polluting lignite coal had fallen 14% vs. the same year-earlier period in the tax’s inaugural nine months, with conventional coal-fired generation also falling, by nearly 5%. During the same period, renewable electric generation “soared” by 28% and electricity output from lower-carbon methane increased by 9.5%. While factors such as greater hydro-electricity availability, flooding of a major coal mine, and implementation of a 20% renewable-energy target probably contributed to the declines in coal use, the 2.4% reported drop in overall electricity generation suggests that the carbon tax played a part.

Overall, reported the Age in the same article, “the emissions intensity of the national electricity market has fallen 5.4 per cent since the carbon price was introduced [presumably over the nine months extending from July 2012 through March 2013], meaning carbon emissions from power generation is [sic] down 7.7 per cent, or 10 million tonnes, from the previous nine months.”

Similar statistics were reported earlier, in Jan. 2013, by “The Australian” newspaper. The “big change in the mix of power” was attributed to “much greater use of renewable energy from hydroelectricity from the Snowy Mountains and Tasmania, and also wind farms.” The same source also said that “The retreat of manufacturing has been a factor, with the closure of the Kurri Kurri aluminium smelter last year and cutbacks in other metals plants affecting industrial demand.” A consultant cited by The Australian added that “the spread of roof-top solar panels and of appliances that used less energy were reducing growth in household consumption” of electricity, while another consultant, pointing to reduced electricity generation and emissions, said that “changes of this scale are without precedent in the 120-year history of the electricity supply industry.”

According to “The Australian,” the power sector accounted for about half of Australia’s emissions and a larger share of the carbon tax, because some of the largest emitters have free permits.”

Use of the carbon tax revenues was complex. Some went to the Australian Renewable Energy Agency for project funding and other monies providing “a raft of other compensation and development funds focused on biodiversity, low carbon agriculture, small business grants and support for indigenous communities,” according to Big Pond Money. More than half of the revenue was said to be earmarked to support low and middle income households to cover the increase in prices that business will pass on to consumers. The government also acknowledged, according to Big Pond Money, that the carbon tax would take more from 3 million households than it would return, while 2 million households would be no worse off and 4 million households better off. A Household Assistance Estimator developed by the authorities was said to provide a means for families to estimate how they would fare financially under the carbon tax.

A later AP story hammered Australia’s carbon tax, asserting that “Voters have never stopped hating the tax and its effect on their electric bills” and predicting that it would doom the ruling Labor Party in the Sept. 8, 2013 elections. “Longtime Labor Party supporters — even people who have helped cut pollution by installing solar panels at home — have flocked to the opposition,” AP reported, in Australian Gov’t Faces Carbon Tax Backlash at Poll (Sept. 6, 2013). “The government estimated the tax would cost the average person less than AU$10 per week,” said AP, “but three months after it took effect, most Australians surveyed by policy think-tank Per Capita said it was costing them more than twice that much. But they also expressed confusion, with most blaming the tax for higher gas prices even though it is not levied on motor fuel purchases.” In an e-mail, cap-and-dividend proponent Peter Barnes blamed the tax’s unpopularity on the absence of “100% dividends, fully transparent and highly visible.” We don’t disagree.

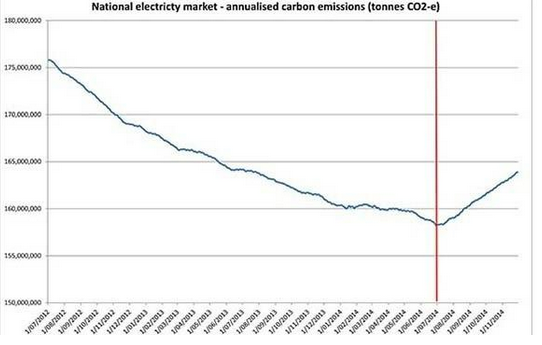

Update (January 2015): In case anyone doubted the effectiveness of taxing carbon pollution, the following graph of power plant CO2 emissions published in Australia’s Guardian shows what has happened in the year since the tax was repealed. The vertical red line is the repeal date.

See also, Emissions for power sector jump as carbon tax ends (Sydney Morning Herald, 1/7/15).

Chile

In October 2014, Chile enacted the first climate pollution tax in South America. It’s a modest levy — a mere $5 per metric ton of CO2 — that applies to only 55% of emissions. Moreover, it doesn’t take effect until 2018. Still, it’s a positive first step. The NY Times reported these details:

Chile’s tax, which targets large factories and the electricity sector, will cover about 55 percent of the nation’s carbon emissions, according to Juan-Pablo Montero, a professor of economics at the Pontifical Catholic University of Chile, who informally advised the government in favor of the tax. At $5 per metric ton of carbon dioxide emitted, Chile’s tax is lower than the $8-per-metric-ton carbon price in the European Union’s carbon-trading system, which has often been criticized as too lax. But it is higher than a carbon tax introduced in Mexico in January.

“We all understand we need to go way beyond the $5 mark” in order to really reduce carbon emissions, Dr. Montero said. However, he added, “I think this still allows you to start building the institutions that you need in the future, when you start moving forward toward more ambitious goals.”

Chile’s tax was enacted as part of a broader tax reform and revenue measure, according to the Times:

Chile’s approval of a carbon tax owes much to its positioning inside a broader tax package, experts said. At the same time that it passed the carbon tax, the Chilean government raised corporate taxes substantially, in a bid to increase revenues for education and other projects. As a result, the carbon tax raised less debate within Chile than it might have otherwise, though electricity companies have objected.

Sweden

Sweden enacted a tax on carbon emissions in 1991. Currently, the tax is $150/T CO2, but no tax is applied to fuels used for electricity generation, and industries are required to pay only 50% of the tax (Johansson 2000). However, non-industrial consumers pay a separate tax on electricity. Fuels from renewable sources such as ethanol, methane, biofuels, peat, and waste are exempted (Osborn). As a result the tax led to heavy expansion of the use of biomass for heating and industry. The Swedish Ministry of Environment forecasted in 1997 that by 2000 the tax policy would have reduced CO2emissions in 2000 by 20 to 25% more than a conventional, regulatory-based policy package (Johansson 2000). On September 17, 2007, Sweden’s government announced that it will increase its carbon taxes to address climate change. Petrol prices will go up 17 öre per litre, with the increase in fuel tax calculated on the basis of a 6 öre tax increase per kilo of CO2 emitted. (The Local)

A new (July 2014) major report by the International Monetary Fund, “Getting Energy Prices Right,” briefly summarized Sweden’s carbon-fuels tax regime as follows:

In the early 1990s, Sweden introduced taxes on oil and natural gas to charge for carbon and (for oil) sulfur dioxide and on coal-related sulfur dioxide and industrial nitrogen oxide emissions. These reforms were part of a broader tax-shifting operation that also strengthened the value-added taxes while reducing taxes on labor and traditional energy taxes (on motor fuels and other oil products). (See Box 3.5, “Environmental Tax Shifting in Practice,” p. 41. The full report is behind a paywall and may be ordered via this link; Chapter 1 of the report, a summary, may be downloaded at no charge via this link.)

Sweden’s carbon tax history and current status were summarized intelligently in a 2013 blog post by “realmelo,” who appears to be a graduate student in economics in British Columbia. Click here for her/his useful, brief report.

Other Nations

(Note: See comment at bottom of page on the Vermont University Law School book, The Reality Of Carbon Taxes In The 21st Century.)

France has no carbon price outside of the implicit price from its participation in the European Union’s Emission Trading System. In April 2016, however, Ségolène Royal, Minister of Environment, Energy and the Sea, issued a four-page declaration calling for the nations of Europe to adopt “a carbon component in the energy tax” of €22/tonne in 2016, with a price trajectory of €56/tonne in 2020 and €100/tonne in 2030. Converting from euros (at the 1.14 exchange rate of 4-April-2016) and metric tons, the price schedule equates to $23/ton today, $58/ton in 2020 and $103/ton in 2030. She wrote:

This measure is essential to encourage energy efficiency and the development of renewable energy in the transport and construction sectors, which have the largest potential for investment and job creation. This change can be made by revising directive 2003/96/CE restructuring the communal taxation framework for energy products and electricity, which has remained unchanged for several years. It may also be undertaken by Member States individually. It should also be based on the principle of fiscal neutrality to avoid increasing mandatory contributions and instead favour the transfer of taxation to fossil fuels. The context is favourable because the drop in the price of hydrocarbons and gas is significant enough so that the carbon component will not result in increasing the final bill including all taxes for consumers (including motorists). Thus, the introduction of the carbon component preserves purchasing power over the short term, but gives a clear signal of the need to quickly carry out energy retrofitting on housing, purchase clean vehicles and develop renewable energy (especially renewable heat and biogas).

Minister Royal’s statement also urged EU member states to “work for the establishment of the carbon price outside the European Union and unite countries that choose to act.”

The goal is not to impose a single worldwide price or a world CO2 market, but to bring together all committed countries and companies around common principles: ensure the carbon price is within the range of between $10-20/tonne before 2020 and $30-80/tonne in 2030; remove subsidies for fossil fuels; prepare for price convergence through networked carbon markets or mechanisms for rebalancing competition such as carbon inclusion mechanisms. The alliance may rely on the Carbon Pricing Leadership Coalition, on condition that it follows its road map and expands it to new countries.

Finland enacted a carbon tax in 1990, the first country to do so. While originally based only on carbon content, it was subsequently changed to a combination carbon/energy tax (U.S. EPA National Center for Environmental Economics). The current tax is €18.05 per tonne of CO2 (€66.2 per tonne of carbon) or $24.39 per tonne of CO2 ($89.39 per tonne of carbon) in U.S. dollars (using the August 17, 2007 exchange rate of USD 1.00= Euro 0.7405). Current taxes are summarized in a Ministry of the Environment fact sheet Environmentally Related Energy Taxation in Finland.

New Zealand made plans in 2005 to enact a carbon tax equivalent to $10.67 (of U.S.) per ton of carbon (based on conversion rate of USD 1.00 = NZD 0.71). The tax would have been revenue-neutral, with proceeds used to reduce other taxes (Hodgson 2005). However, a new government determined that the carbon tax would not cut emissions enough to justify the costs, and the tax was abandoned (Myer 2005). [CTC addendum: In Sept. 2007 the government unveiled a proposed emissions cap-and-trade scheme intended to cover all carbon emissions. The NZ Green Party’s preliminary assessment provides some details.]

We can have carbon border adjustments without being complicit in colonialism

This guest post is by Daniel Ambrosio, a development finance professional working in New York.

The European Union’s massive new economic recovery plan “is notable,” says Harrisburg University engineering professor Arvind Ravikumar, “for its focus on climate action, sustainable investments, and a just transition fund.” Writing in MIT Technology Review, Ravikumar applauds the EU’s €1.8 trillion ($2.1 billion) Covid stimulus package for putting climate policy front and center. Yet he takes aim at the Carbon Border Adjustment Mechanism that is a key component of the plan.

Monument to 17th Century British slave trader and member of Parliament Edward Colston in Bristol (U.K.) is toppled in June.

Ravikumar’s article, Carbon border taxes are unjust, calls Carbon Border Adjustments “colonial” and “a form of economic imperialism” because they reinforce the West’s historic irresponsibility in generating emissions both at home and abroad. In his view, carbon border taxes also fortify Western-based corporations’ ongoing, destructive investment in extractive fossil fuel infrastructure throughout the less-developed world.

It is true that by themselves Carbon Border Adjustments do not address these issues. But does that omission disqualify them? Must correcting historic inequities be a requirement for any and every aspect of climate policy?

Carbon Border Adjustments

A Carbon Border Adjustment is a tax on imports based on the carbon emissions of their production — more precisely, based on the difference between respective carbon tax rates in the importing country and the producing country. If an importing country is taxing its own carbon emissions at, say, $100 per ton of CO2 while the producing country’s tax is just $20, the importing country may impose a Carbon Border Adjustment of $80 on each ton of CO2 ascribed to manufacture of the imported product.

In effect, Border Adjustments supplement a local tax on carbon emissions “production” with a tax on local emissions “consumption” produced abroad. A properly designed (and WTO-compliant) border adjustment thus holds local and foreign producers to a common standard. As both Ravikumar and the EU note, this is necessary to prevent “leakage” of industrial emissions production to untaxed jurisdictions.

Leakage risks are not hypothetical. As Ravikumar notes, “globalization helped the developed world shift manufacturing and outsource its associated pollution burdens to China and other developing countries.” Systematic exemption from Western regulatory regimes for pollution, health and safety and social safety nets powerfully abetted concentration of carbon pollution in the developing world, with myriad local air and water pollution impacts. Yet Ravikumar’s article makes no mention of the possibility that developing countries might foster their own energy transition with carbon taxes, at which point EU border adjustments on imports from these countries would be moot.

A carbon tax on a marginal ton of CO2-equivalent emissions reflects historic untaxed emissions. In other words, because emissions have only just begun to be taxed, returning atmospheric concentrations to pre-industrial levels (or at least capping their rise, as is the EU’s aim, i.e., net carbon-neutral by 2050) requires a tax which internalizes not the damage of a ton of CO2 in isolation, but the damage of that additional ton in the specific context of atmospheric concentrations as they are and the distance needed to travel to meet targets.

Criticism of this approach is correct in that it is blind to 1) who caused the damage to this point, 2) how well situated an individual, firm or nation is to cope with the cost internalization, and 3) the degree of agency these individuals, firms and nations have over their emissions levels. However, the incidence of this taxation — who ultimately bears its burdens — is only one facet of how the costs are ultimately borne.

Disentangling Price Signals and Climate Justice

Many carbon tax proposals and implementations are committed to revenue neutrality. The intent is to price emissions and thus create an economy-wide impetus for behavioral and structural changes while holding average cost of living in place. And while revenue-neutrality does not directly address the international legacy emissions problem, it at least does not exacerbate it.

Global inequity can be addressed through use of carbon border revenues or separate climate reparations such as wealth transfers, technology transfers, concessional financing, and reduced trade barriers. Ravikumar notes, “The Green Climate Fund — established as part of the Paris [climate agreement] — is a good start, but it is not sufficient, nor has it been fully endowed.”

Revenues from carbon border adjustments could fill the funding gap. The broader point is that imposing carbon border adjustments does not preclude addressing international climate justice. Putting a price on carbon that limits regulatory arbitrage and thus discourages emissions leakage is the single most equitable way to distribute the price signals that drive low-carbon investment and behavior. It is also almost certainly a sine qua non to overcome trade-union and other worker-based opposition to carbon taxing in the U.S. and other industrial nations.

Ravikumar’s article advances its own intriguing proposals for climate equity:

Reforms to WTO rules should allow developing countries to grow a domestic green manufacturing sector without triggering a WTO dispute. Developed countries and global financial institutions should extend access to low-interest financing, as well as to technology transfer and bilateral trade and exchange programs that help build capacity for climate mitigation and adaptation in developing economies.

None of these is incompatible with a carbon taxing and border adjustment scheme. Nevertheless, given how repeatedly the article decries “colonialism,” it is worth nothing that each of Ravikumar’s proposals reflects a top-down approach likely to advantage firms with political clout, at least compared to the impartial approach of broad carbon pricing.

The article does bring to the surface a number of important considerations as the EU develops its Carbon Border Adjustment Mechanism through consultations. However, its animus toward Border Adjustments appears misplaced.

Green New Dealers Should Embrace a Carbon Tax

CTC policy associate Bob Narus wrote last month that Carbon Tax Advocates Should Embrace a Green New Deal. Here is his mirror-image brief for including a robust carbon tax in a Green New Deal.

The Green New Deal isn’t a policy yet. Right now, it’s mostly an aspirational slogan and a set of bullet points, which is fine for the moment. There’s time to work out the policy details. But it’s important that a robust carbon tax become one of those bullet points, because without it no deal, no matter how new and green, can do everything we need to do to prevent global climate change from spinning out of control.

Rally in Victoria, BC, March 2019. Photo courtesy of Anne Hansen.

Whether a carbon tax is part of the Green New Deal depends on whose Green New Deal you mean. The Data for Progress report, A Green New Deal — essentially Document Zero for the Green New Deal movement — doesn’t endorse a carbon tax but does note that “there is new analysis that a carbon tax will not hamper the economy, particularly as revenues are reinvested smartly in communities.”

The Alexandria Ocasio-Cortez/Ed Markey resolution, H.R. 109/S.R. 59, doesn’t mention a carbon tax, or any other potential source of funding for its ambitious goals, but AOC herself has publicly recognized the need for taxes to internalize the externalities of some industries or markets.

The policy details will fall into place over time. In particular, one hopes the many Democratic presidential candidates who have endorsed a “Green New Deal” will say more about what they mean by that — which policies they would include, what they’ll cost, how to pay for it all.

In short, we will have a national conversation about the Green New Deal. To everyone engaged in that conversation, here’s a quick take on why a carbon tax should be part of it:

1. If you believe the IPCC, we have to do everything.

In its most recent report, the IPCC called for roughly halving (from 2010 levels) world carbon dioxide emissions by 2030. Achieving that in the U.S. would require a 5 percent annual decrease in carbon emissions from fossil fuels, which would quadruple the actual rate of decline from the mid-aughts to 2017 (see technical note at end). And right now we’re going in the wrong direction: The Rhodium Group estimates that U.S. CO2 emissions rose 3.4 percent in 2018.

With a challenge like that ahead of us, we can’t afford to take any option off the table. As I argued recently, a carbon tax alone will not do the job. But neither will anything else. We need to throw everything we’ve got at the climate crisis, and that definitely includes the most economically efficient tool.

2. A carbon tax will make everyone a partner in the effort.

Addressing the climate crisis is going to demand a heavy dose of government intervention in the economy. But it will require more than that. A carbon tax will deliver economy-wide impact, giving every business and household incentives to change how they produce things and what things they buy. Getting the job done will take billions of dollars in public investments and millions of smaller decisions in the marketplace. A carbon tax will make more of the latter happen.

3. A carbon tax can affect industries that are hard to regulate.

There’s no question that performance standards and other regulations must be a major part of climate policy. But not everything lends itself to such regulation. As energy analyst Hal Harvey explained to Vox’s David Roberts late last year:

It’s hard to set a performance standard that works for glass, pulp and paper, steel, chemicals, and so forth. So in those realms, setting a price is a nice way to handle it. Then businesses can simply internalize the costs and make better decisions.

4. A carbon tax makes everything else we need to do easier.

Want to subsidize renewables? Higher fossil fuel prices will allow smaller subsidies to close the cost gap between carbon-based and renewable power. The same amount of spending on subsidies will then bring more renewables online.

Want to incentivize clean energy investments, like energy efficiency? Higher fossil fuel prices shorten the payback period on those investments. Again, we’ll be able to reduce the degree of subsidies or other inducements required to get households and businesses to make those investments.

Carbon taxes can even replace some regulatory efforts. Citizens’ Climate Lobby argues that its fee-and-dividend proposal could reduce emissions in the power sector more and faster than President Obama’s Clean Power Plan proposal. That means regulatory efforts could concentrate instead on sectors, like transportation and buildings, that are less responsive to energy pricing signals than power generation.

5. A carbon tax can affect emissions beyond our borders.

It’s not enough to reduce U.S. emissions. The rest of the world must do its part. (Of course, right now the rest of the world is saying that about us.) A carbon tax with a border adjustment can pressure other countries to impose their own robust carbon pricing measures. The border adjustment adds a fee to imports tied to the level of carbon emissions required to make that product. (This is, admittedly, not an easy thing to do. Adele Morris of The Brookings Institution treats the complications in a policy brief.)

The border adjustment would be waived on imports coming from countries with carbon pricing equivalent to ours. Each country would face a choice: Pay the U.S. a border adjustment on your exports, or pay yourself the equivalent amount via a carbon tax. For countries that export to the U.S. market, that shouldn’t be a hard decision.

6. A carbon tax will raise revenue that can be used for other climate mitigation programs.

A Green New Deal will create lots of jobs primarily by spending lots of money — rebuilding the power grid, subsidizing clean energy, retrofitting buildings, redesigning cities to be less automobile-dependent, creating an infrastructure to recharge electric cars, etc. That money comes from somewhere, and a carbon tax is a logical source of funds — especially a robust tax that would, in the out years, bring in hundreds of billions of dollars per year.

This is only half an argument for a carbon tax, however, because there are reasons based in economic justice to use the revenue differently. Any carbon tax will hit low-income households proportionally harder than high-income ones, and some or all of the revenue ought to be used to offset the tax’s regressive effects. Fortunately, there are many progressive funding streams — including taxes aimed at high incomes, wealth, or financial transactions — for raising the revenue to fund a Green New Deal. But if the only politically practical way to pay for a Green New Deal requires some carbon tax revenue, the revenue will be there.

* * *

A carbon tax was never an easy sell on its own, and it won’t be an easy sell as part of a Green New Deal either. David Leonhardt at The New York Times just posted a good history of its difficult political fortunes, and comes down about where we are:

The better bet seems to be an “all of the above” approach: Organize a climate movement around meaningful policies with a reasonable chance of near-term success, but don’t abandon the hope of carbon pricing. Most climate activists, including those skeptical of a carbon tax, agree about this.

Carbon tax advocates should take this call to heart. Even with a Democratic takeover in 2020 — which is no sure thing — the U.S. is some years away from either a Green New Deal or a carbon tax. We should use that time to make sure the ultimate answer is “both.”

Here’s how we calculated our figures in the first numbered paragraph: CTC’s carbon-tax spreadsheet model (downloadable Excel file) puts U.S. CO2 emissions from fossil fuels at 5,409 million metric tons (MMT) in 2010 and 4,992 MMT in 2017. With Rhodium’s 3.4% one-year increase, emissions were 5,162 MMT in 2018. To cut that to 2,704 MMT (half of 2010 emissions) in 2030 requires a 5.2 percent annual drop (calculated by exponentiating 2704/5409 to the 1/12 power – 12 years – which is 0.948). A similar calculation from 2005 emissions of 5,822 MMT to the 2017 figure of 4,992 MMT yields an average annual drop of 1.3% over those 12 years.

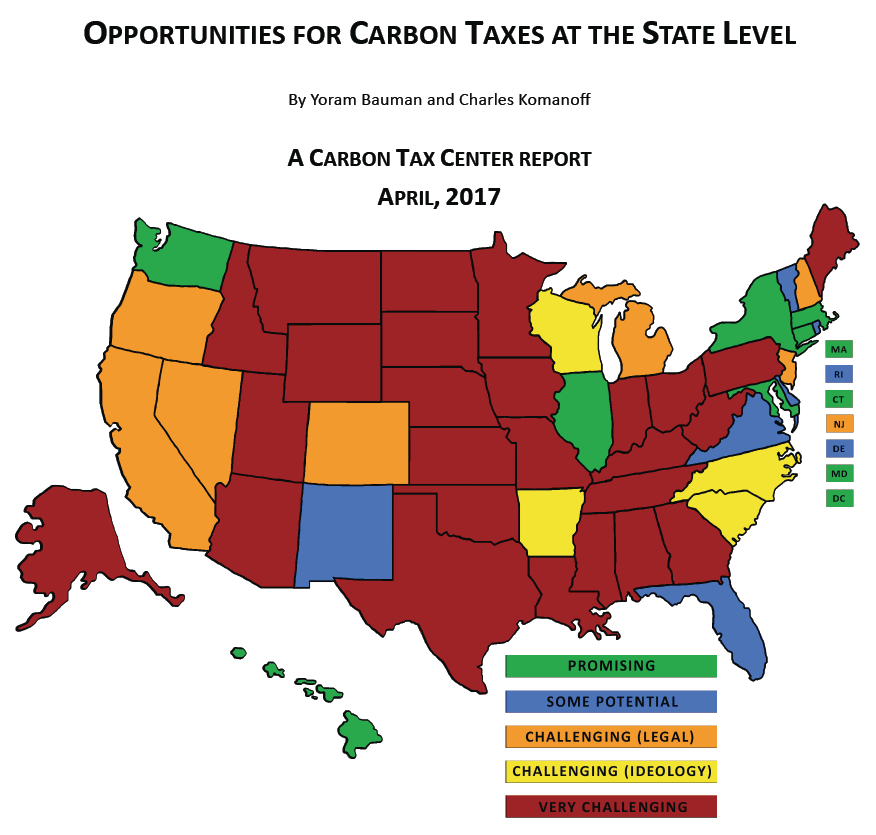

State Carbon Taxes: Overview

No U.S. state has a carbon tax. This fall, carbon tax proponents in the state of Washington are seeking to break through with Initiative-1631, a state tax on carbon emissions, which you can read about here. For a deep dive into the factors that defeated Washington’s 2016 carbon-tax ballot initiative I-732, click here.

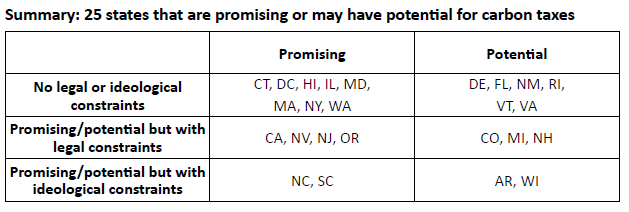

Washington and 7 other states (including Washington DC, which we refer to here as a state) were deemed “promising” arenas for enacting state carbon taxes, in a comprehensive 2017 report by the Carbon Tax Center.

Another page, The Other 49 States, looks at state carbon tax organizing in a half-dozen other states.

CTC Report Ranks the States on Carbon Tax Potential

The report was written by Yoram Bauman, who spearheaded a Washington state carbon tax effort in 2016, and Carbon Tax Center director Charles Komanoff. It classifies the 51 states into five categories of carbon tax readiness ranging from “promising” to “very challenging.” (See map.)

Cover page of CTC’s new report rating the states’ carbon tax potential.

As the map shows, the eight most promising states are Connecticut, Hawaii, Illinois, Maryland, Massachusetts, New York, Washington and the District of Columbia. (Follow these links for historical perspective and other information on Massachusetts, New York, and Washington that isn’t in the report.) We rate another 17 states as having “potential” for enacting state carbon taxes, with some having relatively clear paths while others appear to face legal or ideological constraints. (Follow these links for additional information on Oregon, Rhode Island, Vermont, and—as a bonus—the city of Boulder, Colorado.)

The other 26 states are a lot less promising. Our report explains why.

The rankings are just one aspect of the report. Each state gets an overview, a brief analysis of CO2 emissions, summaries of local climate impacts and current climate policies, a sketch of carbon pricing activism, a brief look at climate ideology and politics, recent polling results, and, where applicable, a summary of ballot measures and proposed legislation.

The report is comprehensive in its coverage but concise in each state’s analysis and ranking. It clocks in at 120 pages, making it huge (a 14 MB pdf), but it’s well worth perusing for info on your state and how it stacks up with others. Click here to download. (A reduced-size pdf under 2 MB is available for those with slower connections, click here.)

Further below is extensive coverage of the Washington state I-732 campaign and its aftermath, along with info on carbon tax organizing in five other states as well as Boulder, CO’s carbon tax on electricity generation. Click on those links and read our introduction for context.

Also see our August 2016 post reporting on the new Brookings Institution report, State-Level Carbon Taxes: Options And Opportunities For Policymakers. It’s essential reading for people seeking to advance carbon taxes at the state level and anyone who wants to understand the nuts and bolts of designing and implementing actual carbon taxes.

State Carbon Taxes: Overview

“It is one of the happy incidents of the federal system that a single courageous state may, if its citizens choose, serve as a laboratory; and try novel social and economic experiments without risk to the rest of the country.” — Justice Louis D. Brandeis (New State Ice Co. v. Liebmann, dissenting opinion, 1932)

This page covers organizing campaigns for U.S. carbon taxing at the state level, with sections on Washington State, Oregon, New York, Massachusetts, Rhode Island and Vermont.

![]() With a national carbon tax blocked by the denialist Republican majority in Congress and a carbon-besotted White House, a growing number of climate advocates are heeding Justice Brandeis’s advice and are organizing at the state level. “Retail” politics, it is thought, might assuage concerns over outside-the-box ideas like carbon taxing, perhaps as occurred in the successful push for marriage equality (the right to same-sex marriage) which began and spread as state-level campaigns.

With a national carbon tax blocked by the denialist Republican majority in Congress and a carbon-besotted White House, a growing number of climate advocates are heeding Justice Brandeis’s advice and are organizing at the state level. “Retail” politics, it is thought, might assuage concerns over outside-the-box ideas like carbon taxing, perhaps as occurred in the successful push for marriage equality (the right to same-sex marriage) which began and spread as state-level campaigns.

Moreover, progressive and popular options for distributing carbon tax revenues can be made more tangible at the state level than the federal. This point was underscored by a Jan. 2015 study by the Institute for Taxation and Economic Policy ranking the 50 states on their tax incidence that established that states are more regressive taxers than the federal government. In particular, sales taxes could be swapped out for carbon taxes, as advocates in Washington State proposed in their I-732 ballot initiative in 2016 (full discussion further below).

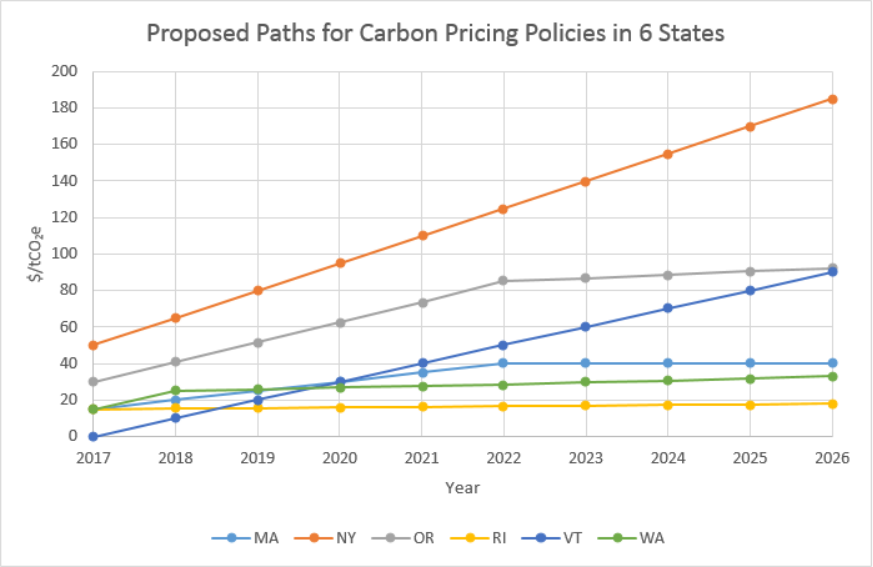

Not all states are riven by ideological resistance. While America’s geographical diversity can impede national unity, it has left some states less beholden to fossil fuel interests. Naturally, advocates are focusing on those states. (In March 2016, Resources for the Future posted two superb summaries of proposals in six states to adopt carbon taxes; the first focused on the tax rates (see graphic below), while the second addressed revenue treatment and household “incidence.”)

Graph courtesy of RFF. See link in adjoining paragraph.

States have also pushed the envelope on issues like minimum wage and fuel-efficiency standards, moving the national discussion as they did so. In a 2016 op-ed in the New York Times, Georgetown University law professor David Cole ascribed the National Rifle Association’s success at strangling national gun-control regulations to a decades-long campaign that changed state constitutions and laws to protect the right to possess and carry guns. Less far afield is the fact that gasoline taxes first took root in a handful of Western states to fund road construction, before spreading to the rest of the country. State carbon taxes could, it is hoped, create a similar template leading eventually to federal enactment.

The EPA Clean Power Plan may have provided an opening for state carbon taxes through a provision allowing states to submit projected emission reductions from carbon taxes applied to power generation (unfortunately, reductions from carbon-taxing non-electric sectors such as transportation would not receive credit). A June 2015 report from the Niskanen Center concluded that even small state carbon taxes could effectuate the required emissions reductions in most cases, mirroring our own modeling results on the national level.

Still, state carbon taxing raises issues that don’t apply to a federal tax. State policy makers and advocates need to address these concerns:

- Competitiveness: It would be hard for any one state to push its carbon tax too high, due to concerns over competitive advantage and inter-state “leakage” (e.g. driving out-of-state to fill up with untaxed gasoline).

Yet using some carbon tax revenues to reduce business taxes (as was proposed in Washington State) may soften concerns over economic impact. The cross-border issue may be less salient in larger Western states than in smaller East Coast states.

Jeff Renfro, a key member of a team at Northwest Economic Research Center that modeled a possible Oregon carbon tax, said:

We tried [in our modeling] to wreck the economy. We modeled a big tax – $100 a ton – with a relatively short phase-in period, and we assumed the government put the revenues toward non-productive reserves. Even in that scenario, we were surprised by how small the effects on employment were relative to the overall economy. (Interview with CTC researcher Matt Gordon, July 10, 2015)

- Efficiency: Energy policy is largely determined at the federal level. Administrative costs could be disproportionately higher for state taxes, due to greater cross-border movements of electricity and fuels among states than between the U.S. and other nations. In some states, utility sector regulation may complicate efforts to tax fossil fuels sufficiently upstream.

Many states already have taxes on gas and electricity, however, and it shouldn’t be difficult to piggyback a carbon tax on those taxes without significantly increasing administrative burdens. British Columbia’s carbon tax program uses this technique, and reports the administrative burden as negligible.

- Coverage: Only a national carbon tax will enable the U.S. to impose Border Adjustment Taxes to induce China and other countries to adopt their own taxes, which is a key benefit of pursuing carbon taxing. States cannot pursue a similar strategy without violating the commerce clause of the Constitution.

Although states may not tax imported goods, that prohibition shouldn’t be construed to mean they can’t tax imported electricity or fossil fuels that are then used within the state. In fact, some advocates see this as an opportunity for economic development; carbon-taxing out-of-state fossil-based electricity and fuels could stimulate growth in local renewables and energy-efficiency industries.

- Local Policy: Every state has idiosyncracies. In Oregon, the constitution mandates that all revenues from taxing gasoline must be deposited in the Highway Trust Fund. In Washington, state law precluded carbon tax revenues from being used for dividends to the public. Yet this patchwork of state policies may be a motivating factor in driving a national policy. The complications of doing business in jurisdictions with varying policies have even driven some oil companies to demand more unified action on climate change.

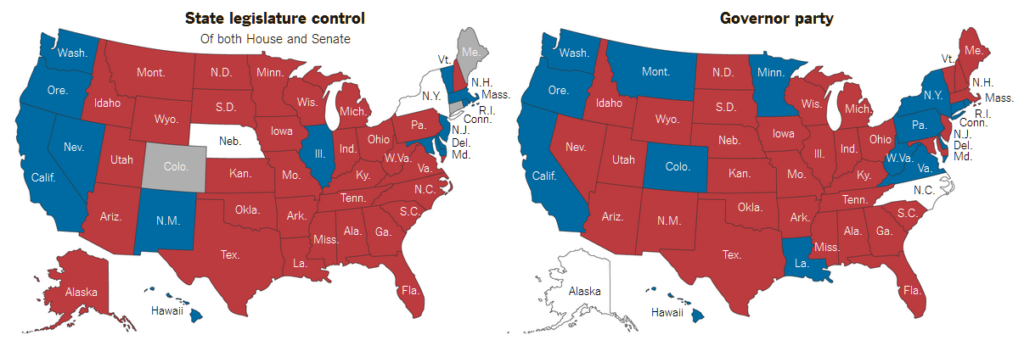

That said, the 2016 elections further cemented the Denier (Republican) Party’s hold on state governments, as the New York Times graphic below illustrates.

Republicans hold control of the governor’s office and the legislature in 24 states, while Democrats have that status in only six, according to this New York Times graphic.

On the other hand, red states tend to be fossil fuel-dominated states already out of reach of state carbon-tax campaigns. Two states with past or present carbon tax organizing, WA and OR, have Democratic governors and legislatures. Two others, NY and CO, have Democratic governors but divided or uncertain legislatures. Massachusetts and Vermont have Democratic legislatures but Republican governors.

Bipartisan Plaudits for Rep. Delaney’s “Tax Pollution, Not Profits Act”

If any climate legislation could garner at least nominal bipartisan support, it might be Rep. John Delaney’s Tax Pollution, Not Profits Act. Delaney is in his second term representing Maryland’s 6th CD, which runs from the DC suburbs to the western end of the state. His proposal, introduced on Earth Day at the American Enterprise Institute in Washington, would tax carbon dioxide and CO2 equivalents from methane and other sources at a rate of $30 per metric ton, increasing annually at 4% above inflation. The measure includes border tax adjustments to protect energy-intensive domestic industry from unfair competition from nations that haven’t enacted carbon taxes.

Rep. John Delaney (D-MD)

Delaney’s measure offers a sweetener to conservatives: a promise to apply roughly half of carbon tax revenues to reduce the top corporate income tax rate from 35% to 28%. The bill would also provide monthly payments to low- and middle-income households and fund job training, early retirement and health care benefits for coal workers. At least as critically, at the AEI unveiling, Delaney committed near-apostasy by suggesting that his carbon tax could substitute for the Obama administration’s Clean Power Plan, final regulations for which EPA issued last month.

The Carbon Tax Center assessed the Delaney proposal’s effectiveness using our 7-sector model. We project that in its third full year the measure’s $30 price would reduce U.S. CO2 emissions to 8% below emissions in the year before enactment. Unfortunately, its schedule of 4% annual real rises is too tepid to continue reducing emissions more than fractionally over the longer term. The low upward price trajectory is a shortcoming shared by the American Opportunity Carbon Fee Act, introduced by Senators Sheldon Whitehouse (D-RI) and Brian Schatz (D-HI) in June.

In contrast, carbon tax proposals introduced in this Congress by Rep. John Larson (D-CT) and Rep. James McDermott (D-WA) would rise briskly to exceed $100 per metric ton within a decade, which we estimate would reduce U.S. emissions below this year’s levels by more than one-fourth in that time (and by nearly a third below 2005 emissions).

In an online discussion forum hosted by OurEnergyPolicy.org, Rep. Delaney asked for comments on his proposal. Below, we group and summarize those comments. [Read more…]

Don’t Anchor a Carbon Tax to the Social Cost of Carbon

Editor’s note: Yesterday the world’s most influential newspaper finally did what CTC and other carbon tax proponents have sought for years: publish a ringing endorsement of a U.S. carbon tax. With its editorial, The Case for a Carbon Tax, the New York Times joins the growing community of opinion leaders, policy experts and, yes, elected officials who not only recognize the power of carbon taxes to quickly and equitably reduce emissions but also sense the emergence of a political critical mass that can enact fees into law. This heartening development signals that it’s not too soon to focus on the design of a U.S. carbon tax, especially its magnitude and rate of increase, as CTC senior policy analyst James Handley does in this post.

Which is the more effective way to set a tax on carbon pollution?

A. Start aggressively, then raise the rate slowly (“sprint”).

B. Start modestly, then raise the rate briskly and predictably (“marathon”).